NEW! Explore the Data-Driven Decisions Lab (D3L)

The Delaware DOJ's Data-Driven Decisions Lab is now live. Access interactive dashboards, reports, and data-driven insights that support transparency, accountability, and evidence-based decision-making.

Learn more

about this alert.

Information in this section includes archival records maintained for public reference. In some cases, these documents and videos below may not be optimized for use with assistive technology. We are committed to ensuring that web content uploaded after April 2026 meets WCAG 2.1 Level AA accessibility standards.

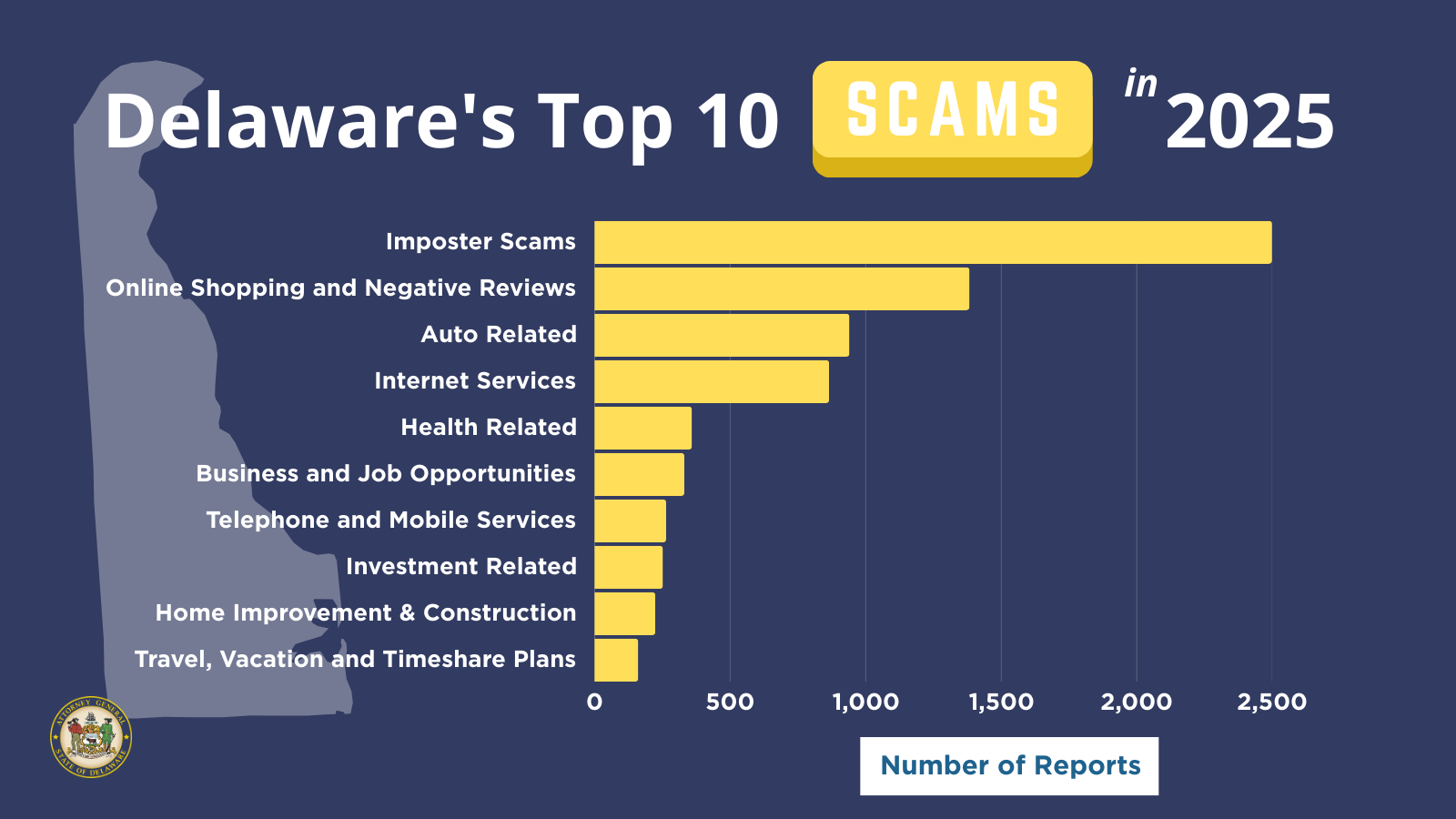

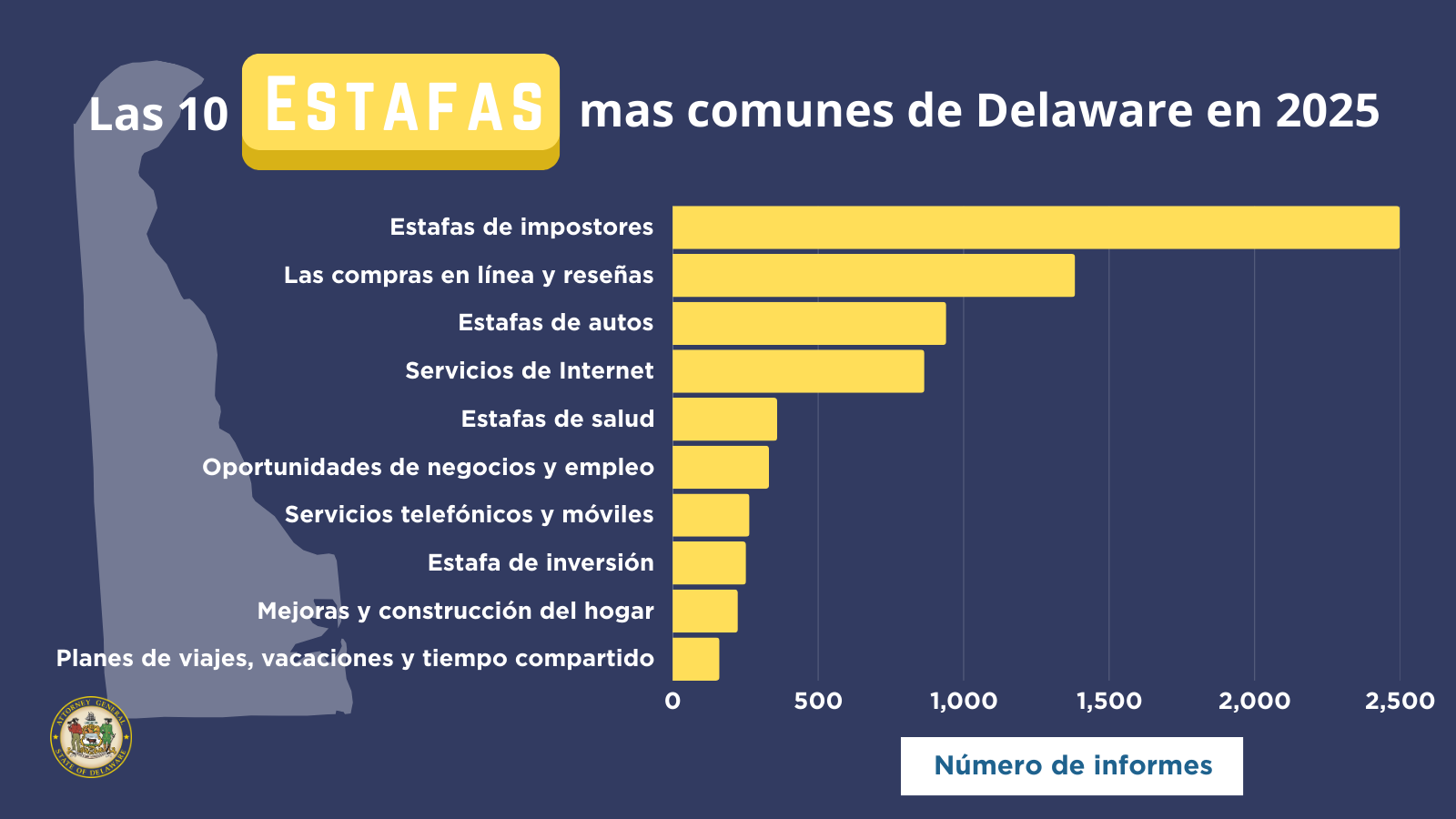

The Consumer Protection Unit identified the Top 10 Scams Delawareans reported in 2025.

If you are a victim of a scam, please fill out a consumer complaint form at de.gov/consumercomplaint or by phone at (800) 220-5424.

Scammers use sophisticated tactics to defraud members of our community, including the most vulnerable among us. But quite frankly, anyone can become a victim of scam. Our Consumer Protection Unit has provided tips and advice for consumers on how to reduce the risk of being scammed. We strongly encourage consumers to visit the Federal Trade Commission and/or the Better Business Bureau of Delaware to learn about different scams and how to report them.

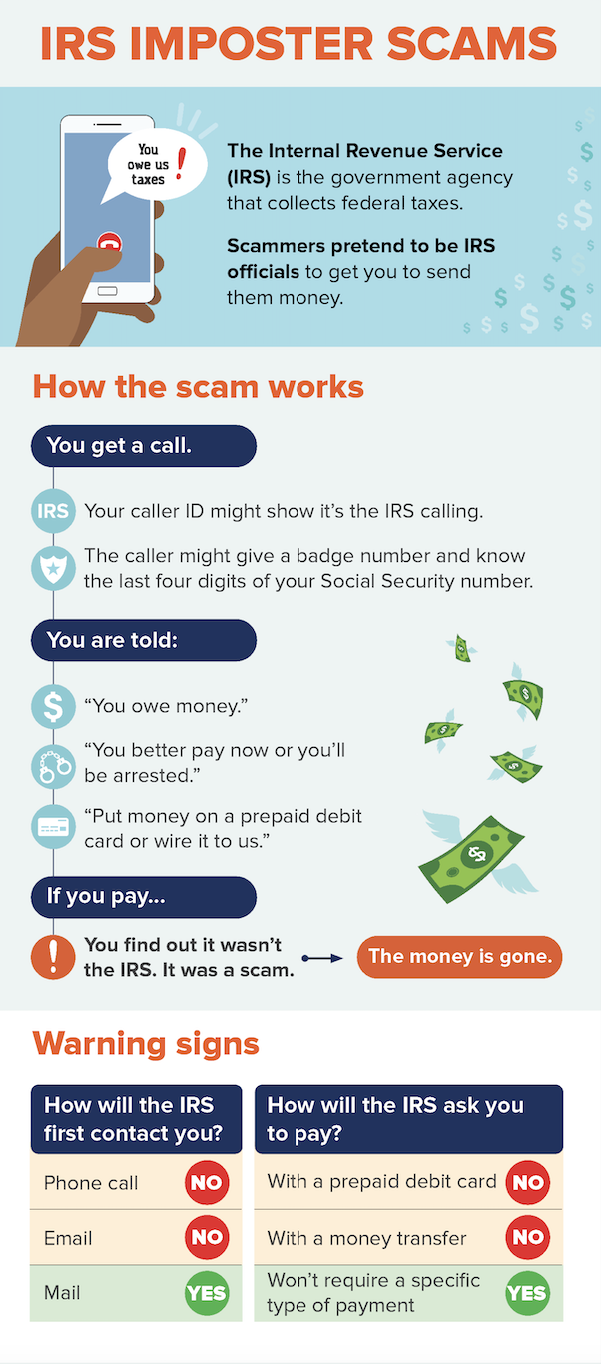

Imposter scams come in many varieties but work the same way: a scammer pretends to be someone you trust to convince you to send them money. Scammers can pretend to be anyone, such as the Internal Revenue Service (IRS), Tech Support, the Social Security Administration, or even a family member.

Here are some tips:

Our Consumer Protection Unit hosted a discussion on imposter scams with DOJ Deputy Director of Consumer Protection Ryan Costa, Better Business Bureau Director of Business Jon Bell, Social Security Administration Public Affairs Specialist Matt Baxter, and AARP Delaware Communications Director Kimberly Wharton. This discussion was moderated by Marion Quirk.

This is an archival video and does not include captions.

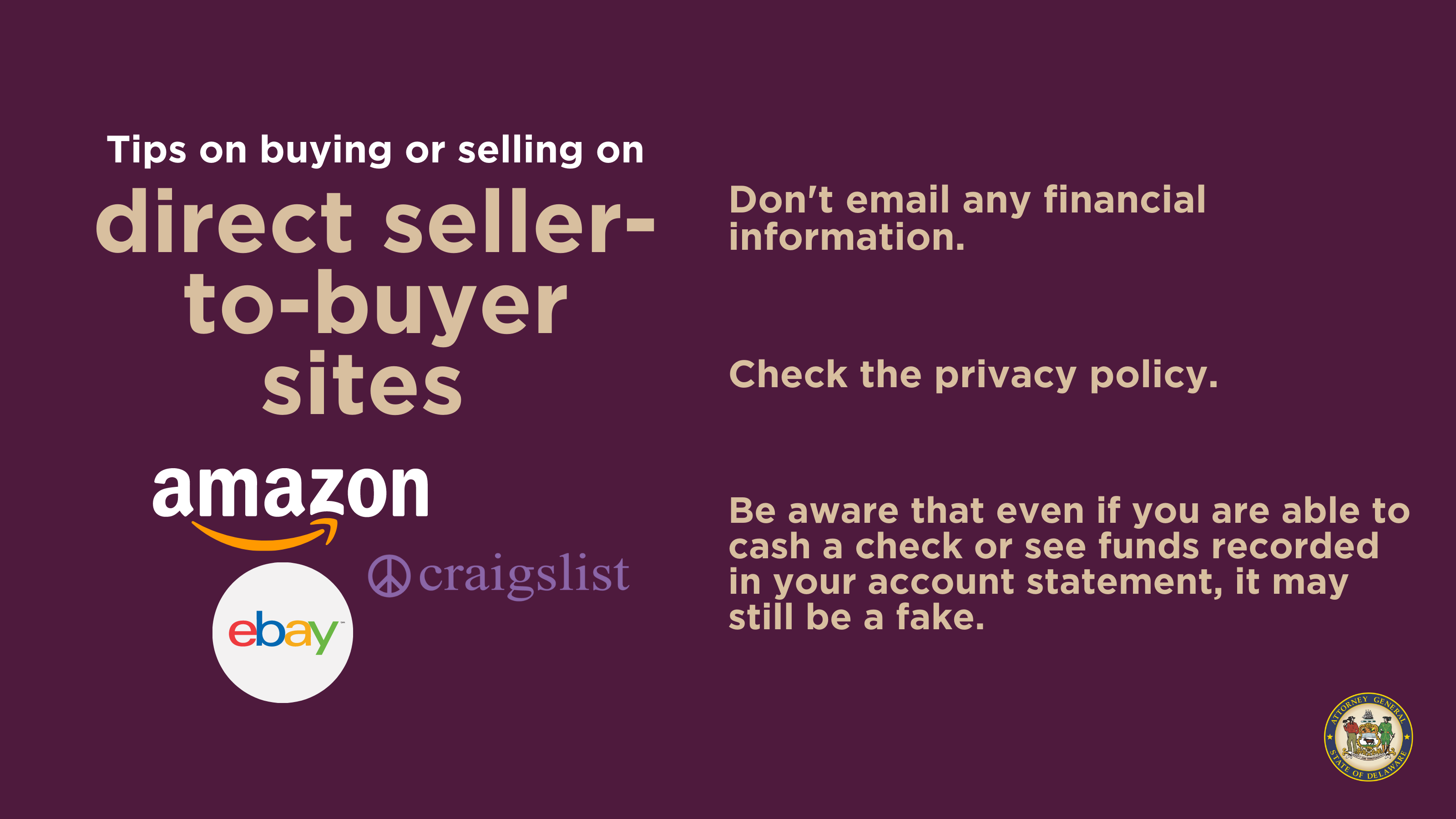

These cons often involve purchases and sales, often on eBay, Craigslist, or other direct seller-to buyer sites. Scammers may pretend to purchase an item only to send a bogus check and ask for a refund of the “accidental” overpayment. In other cases, if the scammer is the seller, they never deliver the goods.

Here are some tips:

If you are buying off direct seller-to-buyer sites, remember:

Don’t email any financial information.

If you begin a transaction and need to give your financial information through an organization’s website, look for indicators that the site is secure, like a URL that begins https (the “s” stands for secure).

Check the privacy policy.

It should let you know what personal information the website operators are collecting, why, and how they’re going to use the information.

Beware that even if you are able to cash a check or see funds recorded in your account statement, it may still be a fake.

If a buyer or seller tries to persuade you to go outside the site’s usual process or payment methods, that’s a big red flag 🚩.

Our Consumer Protection hosted a discussion on online shopping scams with DOJ Special Investigator LaVincent Harris, and Better Business Bureau Director of Business Jon Bell. This chat was moderated by Gina Schoenberg.

This is an archival video and does not include captions.

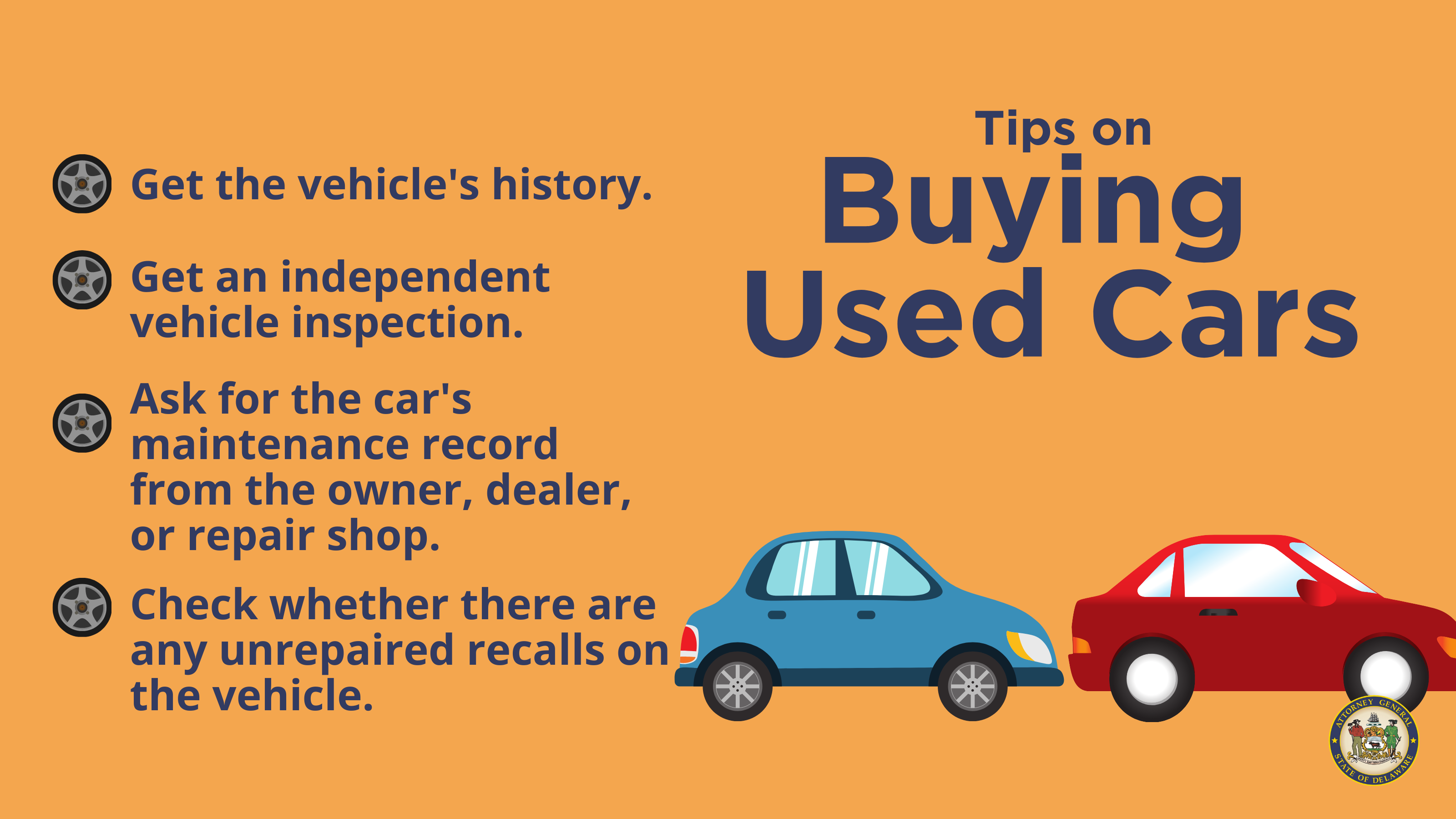

These complaints can include selling cars that have undisclosed problems or selling extended warranties but refusing to cover expenses. Additionally, car dealerships may put tempting deals in their advertisements, but when you try to close the deal, the deal is not what it looks like.

Here are some tips:

Get the vehicle’s history.

➡️ Visit the National Motor Vehicle Title Information System (NMVTIS) website at vehiclehistory.gov to get a vehicle history report with the title, insurance loss, and salvage information.

Get an independent vehicle inspection

to ensure it doesn’t have hidden damage.

Ask for the car’s maintenance record from the owner, dealer, or repair shop.

Check whether there are any unrepaired recalls on the vehicle.

You can check yourself by entering the VIN at safercar.gov, or by calling the National Highway Traffic Safety Administration (NHTSA) Vehicle Safety Hotline at 1-888-327-4236.

If you get mail or phone calls about renewing your vehicle warranty, don’t take the information at face value.

Be alert to telemarketers pitching auto warranties using high-pressure tactics to hide their true motives. Most legitimate businesses will give you time and written information about an offer before asking you to commit to a purchase.

Be skeptical of any unsolicited sales calls and recorded messages.

If your phone number is on the National Do Not Call Registry, you shouldn’t get live or recorded sales pitches unless you have specifically agreed to accept such calls.

Report violations or register a phone number to the National Do Not Call Registry at DoNotCall.gov or call 1-888-383-1222.

Our Consumer Protection Unit hosted a discussion on auto-related scams with DOJ Deputy Attorney General George Lees, DOJ CPU Special Investigator LaVincent Harris, and Division of Motor Vehicles Chief of Compliance and Investigations Karen Carson. This chat was moderated by DOJ Paralegal Diana Anderson.

This is an archival video and does not include captions.

These scams use Internet services or software with Internet access to defraud victims or to otherwise take advantage of them. Internet crime schemes steal millions of dollars each year from victims and continue to plague the Internet through various methods.

People spend billions of dollars a year on products and treatments in the hope of improving their health and fitness. A lot of that money goes to companies that make fake claims about those products and treatments, cheating people out of their money, time and even their health. (FTC Definition)

These scams target consumers regarding mobile plans, rates or coverage areas, problems with mobile applications or downloads, unauthorized switching of consumers’ phone service provider, misleading pre-paid phone card offers, VoIP service problems, electronic consumer products such as smart watches, and connected-home devices that can connect to the internet and use a processor or sensors to collect consumer information. Learn more about how to spot and report a tech scam.

Common scams that lure you in with promises of making a lot of money quickly, easily, and with low risk – usually by investing in the financial or real estate markets. (FTC Definition)

Home improvement contractors who promise to do the work on your home but end up leaving you and your home worse off than when it started. For example, starting a project and not finishing, damaging your home, overcharging you, or simply just taking your money and not doing any work. (FTC Definition)

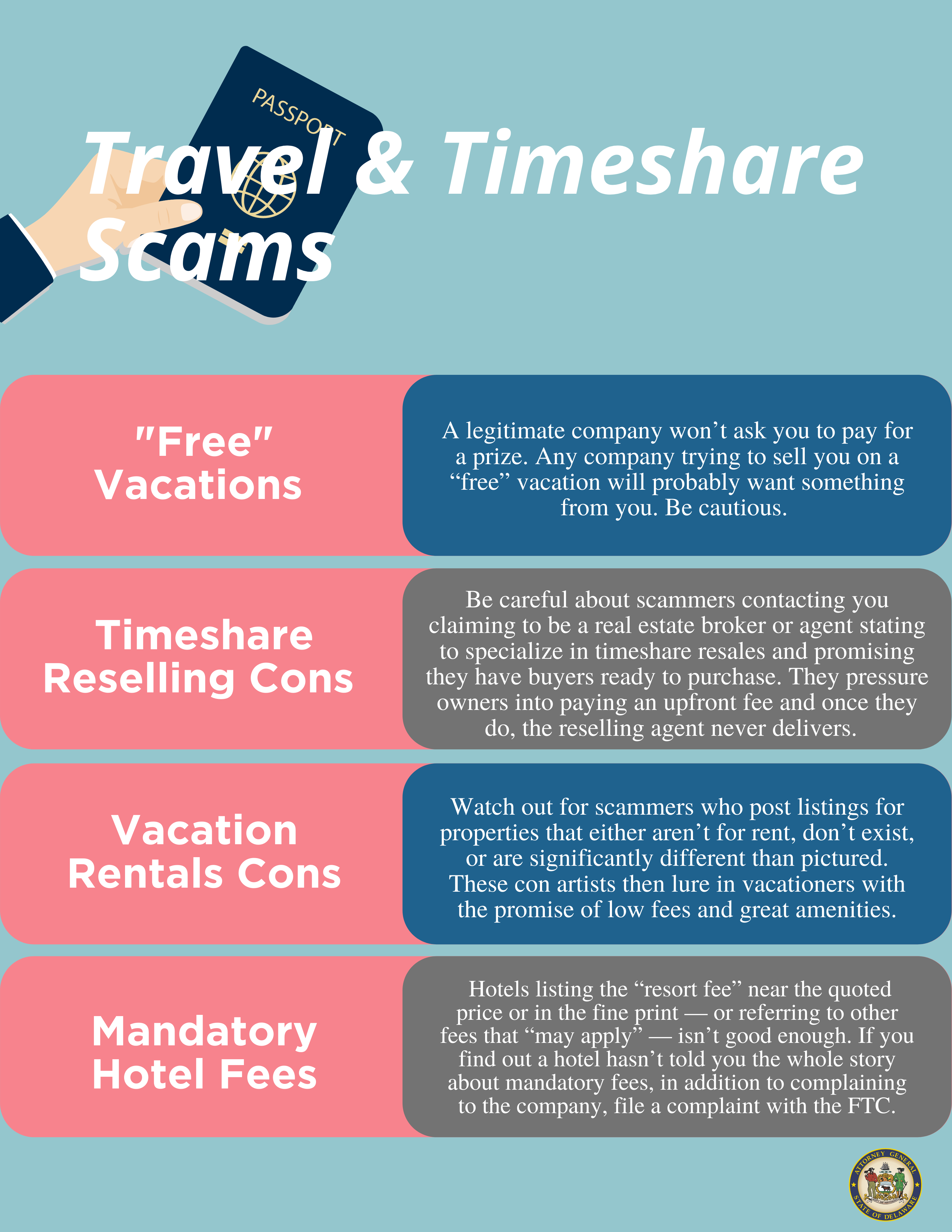

Listings are posted for properties that are not for rent, do not exist, or are significantly different from what’s pictured. In another variation, scammers claim to specialize in timeshare resales and promise they have buyers ready to purchase.

Here are some tips:

“Free” vacations.

A legitimate company won’t ask you to pay for a prize. Any company trying to sell you a “free” vacation will probably want something from you. Be cautious.

Timeshare reselling cons

Be careful about scammers contacting you claiming to be a real estate broker or agent stating to specialize in timeshare resales and promising they have buyers ready to purchase. They pressure owners into paying an upfront fee and once they do, the reselling agent never delivers.

Vacation rentals cons

Watch out for scammers who post listings for properties that either aren’t for rent, don’t exist, or are significantly different than pictured. These con artists then lure in vacationers with the promise of low fees and great amenities.

Mandatory hotel fees

Hotels listing the “resort fee” near the quoted price or in the fine print – or referring to other fees that “may apply” – isn’t good enough. If you find out a hotel hasn’t told you the whole story about mandatory fees, in addition to complaing to the company, file a complaint with the FTC.

Our Consumer Protection Unit hosted a discussion on travel, vacation, and timeshare scams with DOJ Director of Consumer Protection Marion Quirk, and DOJ Deputy Attorney General Jordan Braunsberg. This chat was moderated by Luke Meyer.

This is an archival video and does not include captions.

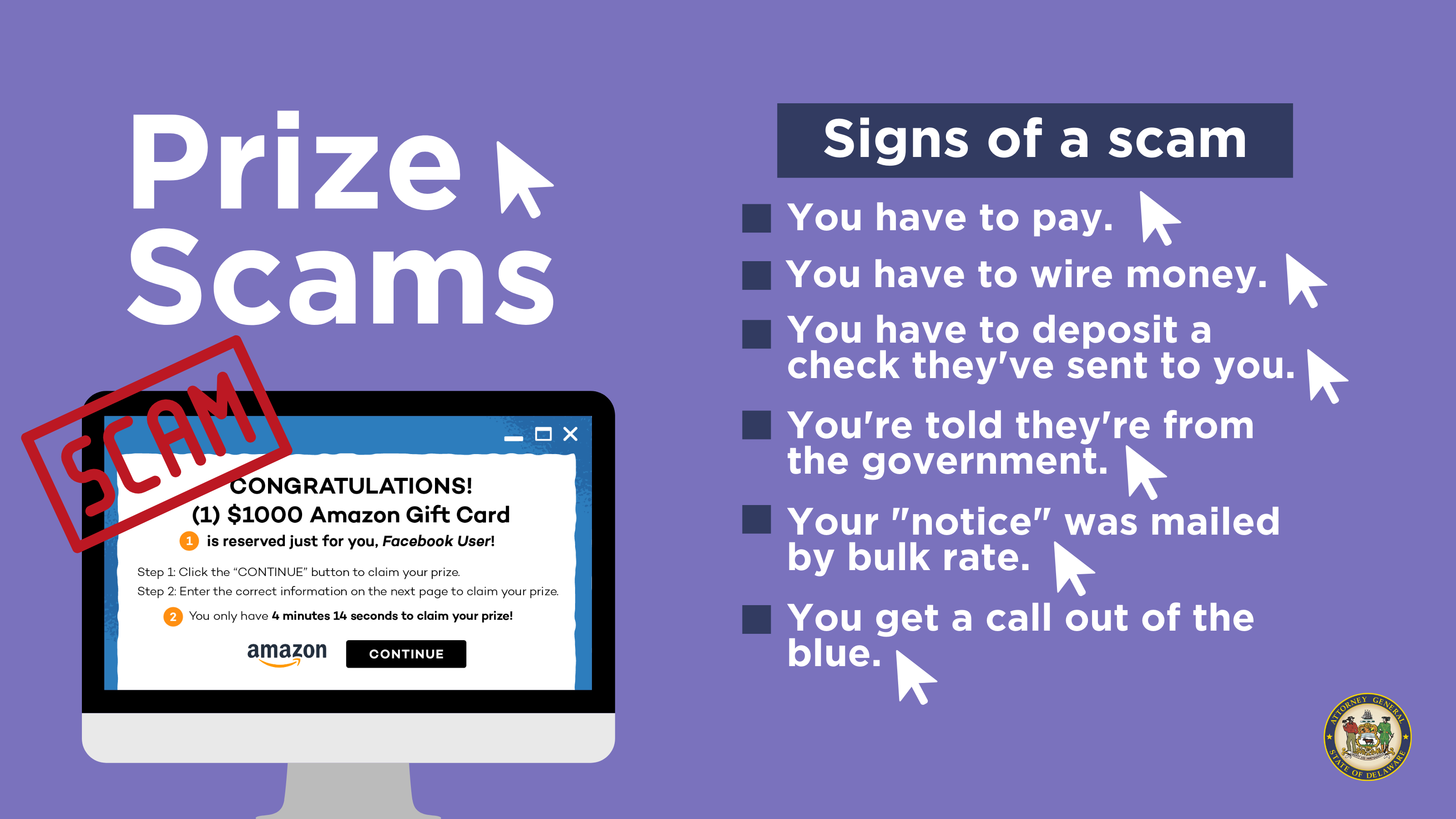

Most sweepstakes scams have a few things in common. They claim that the recipient has won, or is about to win, a large cash prize. And they try to get the recipient to pay money, often supposedly to claim the bogus prize.

Here are some tips:

Signs of prize scams:

➡️ You have to pay.

➡️ You have to wire money.

➡️ You have to deposit a check they have sent to you.

➡️ You are told they are from the government.

➡️ Your “notice” was mailed by bulk rate.

➡️ You get a call out of the blue.

Signs of a lottery scam:

➡️ You did not enter a lottery, but you receive a notice or call from a person claiming to work for the Delaware Lottery.

➡️ You receive a notice or call informing you that you have won a lottery in another country.

➡️ You receive a notice or call informing you that you have won a sweepstake, but you need to pay a fee in order to claim your winnings.

➡️ You receive a notice or call from a person claiming to work with the federal government or a “Federal Sweepstakes Board.”

Our Consumer Protection Unit hosted a discussion on prizes, sweepstakes, and lottery scams with DOJ Chief Special Investigator Alan Rachko, and AARP Delaware Communications Director Kimberly Wharton. This chat was moderated by Gina Schoenberg.

This is an archival video and does not include captions.

Safeguard your information by shredding personal documents (bank statements).

Be alert to impersonation schemes.

Set up alerts on your accounts so you are notified of suspicious charges.

Look at your bank statements and credit card statements for unauthorized charges.

Check your credit report annually for any fraudulent activity.

What do the fraudsters commonly do with your personal information once stolen?

Open credit cards in your name.

Take out loans in your name.

Sign up for unemployment benefits in your name.

Sign up for social security benefits in your name.

How do you know if your identity is stolen?

You receive notice in the mail from a collection agency, credit card company, or other business (all of which you do not have accounts with) stating that you owe them for a past due bill.

You receive an email/text alert advising you of fraudulent credit card charges.

When checking your bank statement or credit card statements, you discover fraudulent charges on your account.

Online Shopping Scams

How do trends and patterns of complaints get analyzed to determine how to escalate and prioritize action?

We have several tools at our disposal to track and analyze trends. We review the statistics generated by those tools on a regular basis and work closely with our federal partners and other state Attorneys General.

How can we submit an inquiry for investigation to the Attorney General’s Office?

If you have any trouble, give us a call: (800) 220-5424

Is there an alert system in Delaware to let consumers know that an online scam has been discovered?

We routinely issue press releases on the latest scams and scam variations. We will also come speak to groups you are associated with about fraud and scams. These outreach events are free of charge and can be offered virtually (only virtual at this time).

What can I do to protect myself? Best tips?

Do your homework.

If the offer is too good to be true, it is likely a scam.

If you are victimized, report it.

Imposter Scams

What are your best consumer tips regarding imposter scams?

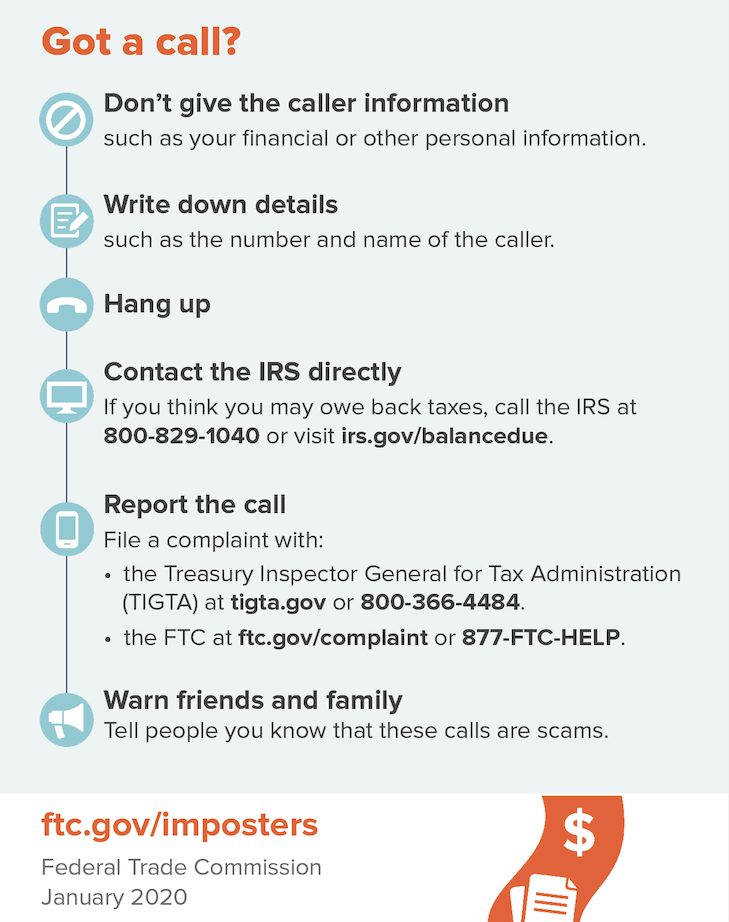

Be suspicious about all links, phone calls, and mailings.

Trust your gut. When in doubt, do not act.

Government entities like the IRS, Social Security Administration, and Medicare will never threaten to arrest you, fine you, or cancel your benefits. Any suggestions that they will is a major red flag.

Always conduct independent verification

Do not use the communication for contact information. Go to an independent source to get contact information. For example, if you receive correspondence from your bank, contact them utilizing the information on your most recent statement or on the bank of your card.

Remember: anyone can make whatever they want appear on your caller ID. You cannot trust your caller ID.

Watch for these red flags

Communications about transactions you do not recall making

Calls to quick action

Requests or demands for money, especially wire transfers and the purchase of gift card or pre-paid cards

Threats of arrest or physical harm

IF IT IS TOO GOOD TO BE TRUE IT IS LIKELY A SCAM.

What should you expect if you file a complaint with the Consumer Protection Unit?

If no loss, we will track the information you provide in our internal and national databases to identify trends, target outreach, and make federal enforcement referrals where appropriate.

If you did experience financial loss, a Special Investigator will reach out to you. If you receive a communication from our office and you are not sure it is real, call us at (302) 683-8800 to verify that the contact is legitimate.

If you file a complaint about a robocall or other phone call, make sure you collect the following information and submit your complaint immediately:

The phone number as it appears on your caller ID

The name, if any, as it appears on the caller ID

The exact time of day that you received the call

Auto Related Scams

How can I protect myself against car repair fraud?

Find a reputable mechanic by asking friends and colleagues for recommendations and checking the BBB for complaints.

You can also utilize AAA; they vet and endorse repair shops, and can help mediate disputes between members and approved shops.

If your check engine light comes on, you can take it to the parts store, and they can run a diagnostic to tell you why the light came on so you can approach your mechanic prepared.

How do I report a complaint to the Better Business Bureau?

The BBB is a great first step when an issue arises; not only can they help consumers address problems they might have with businesses, but they also publish complaints they receive, which can help other consumers, too.

Prizes, Sweepstakes, and Lottery Scams

What are the red flags that I might be dealing with a scam?

You get a notice that you won but you never played.

You are told that you must pay upfront fees and taxes before they can award your prize.

Claims that you have won “unclaimed” winnings.

What should I do if I have been victimized?

File a complaint with our office and the FTC.

Any other tips?

Take advantage of services through your phone provider to block spoofed or manufactured phone numbers.

Remember: anyone can pay for a mailing or an internet ad. Having these things does not make an entity legitimate.

Before you act, call a family member, friend, or us. Talk to someone about what is going on.

Consumer Credit Scams

What can we expect to see in 2021 in terms of consumer credit scams?

Unfortunately, we expect to see folks really struggling with credit—we’re expecting to see an uptick in scams relating to consumer credit as a result.

Where can viewers make a complaint if they are concerned about an unfair mark on their credit report or a debt relief company?

Start with the company itself. Reputable organizations care about correcting their mistakes and keeping their customers happy.

Report it to CPU! We need patterns to act most efficiently.

Is there anything businesses should be aware of in terms of phishing?

Most people think phishing could only happen to individuals, but businesses are just as much at risk to phishing scams as individual consumers are.

There is an entire subcategory called the Business Email Compromise, which can be extremely sophisticated.

Just as you are in your personal life, when you’re at work or you own a business, be on the lookout for phishing emails. Train your employees on phishing scams and how to spot them.

How can you spot a tech support scam?

If you ever receive a text or call from a number that claims to be a company such as Apple or Microsoft, you should immediately think of it as a scam. Legitimate companies will not be contacting you about a potential tech issue.

As super red flag is when someone asks you to pay them using a means that is not typical money, such as Bitcoin or Gift cards.

Travel, Vacation, and Timeshare Scams

What should you do before signing up for a timeshare?

Similar to vacation rentals, do your research! Make sure that the company that is selling the timeshares is legit. If it is a Marriot timeshare, make sure it is actual Marriot selling the timeshare.

Additionally, ensure that the paperwork matches what the promotional information says. Be sure you know what the contract that you’re signing says, regardless of what the salesperson told you.

Never send money/pay for a timeshare before you’ve signed the contract. There is no need to pay money before you sign.

What if you’ve put in for a vacation contest and you’re told you have won, but you’re not sure if it is actually true?

Three avenues:

Cross-reference the contact information for the vacation contest and the contact information of the person who contacted you to let you know you’ve won. If they’re different, that’s a red flag. And reach out to the company that the contest is with.

If there are hotels or resorts involved, independently contact that hotel/resort to make sure the contest is legit.

If there is travel involved (airplane, train, rental car, etc.) independently contact that hotel/resort to make sure the contest is legit.

How can you research a rental company?

Check with the Better Business Bureau to see if the company has gotten any complaints in the past

Check the company’s social media pages to see how they represent themselves.

Check reviews online! If someone had a bad experience, they’re likely to post about it online.

What can you do if you think you’ve been a victim of a rental scam?

Three steps:

Reach out to your banks/financial institutions. Make sure they are aware that you have been a victim of a scam. This should, hopefully, stop future problems.

Gather information about the scam

Make a decision if you are going to follow up with law enforcement. You can file a police report, file a complaint with the BBB or the FTC, or file a complaint with our office.

What information is helpful to report rental scams?

Contact information (phone number, email, name of contact, or company).

Screenshots of your communications (emails, texts, documents you signed).

Timeline of the scam – when you were first contacted to when you realized it was a scam.